The Asterès firm is today releasing a study carried out for ALILA, a promoter specializing in Housing for All, on the impact of Vefa and social housing to meet the housing needs of the French population.

This study entitled "Building more social housing thanks to the VEFA: a pragmatic solution to the Housing Crisis" makes it possible to specify the form that the major housing crisis that France has been undergoing for decades has taken:

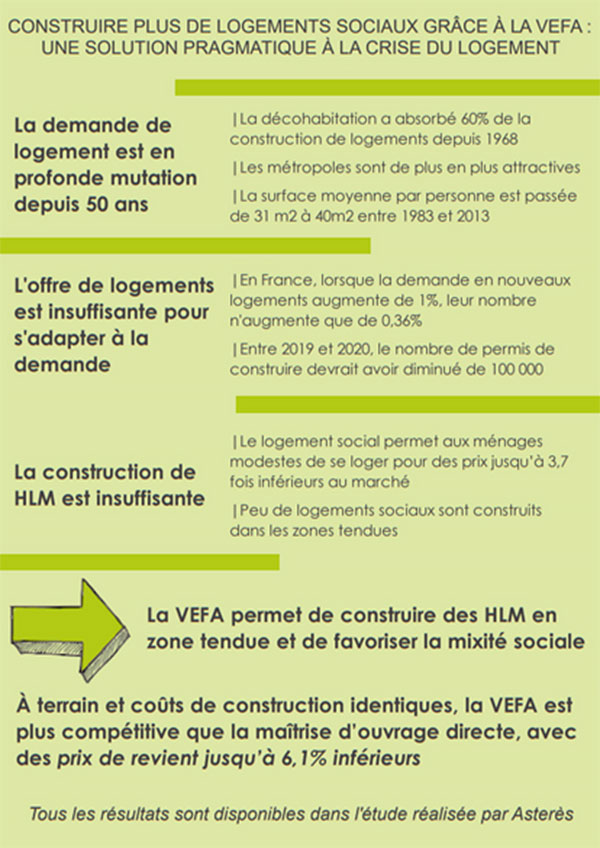

- The housing crisis, multifaceted, is linked to the profound change in demand over the past 50 years: development of decohabitation (decrease in the number of people per household) which has absorbed 60% of construction, concentration of jobs and therefore needs for housing in certain areas, seeking more comfort which attracts the population to certain regions and more spacious accommodation.

- The housing supply is not growing fast enough to adapt to demand, especially in tight areas.

- Housing prices (+ 114% from 2000 to 2019) rise faster than household income (+ 51% from 2000 to 219).

The study shows that to cope with these crises:

- The development of social housing is essential because it allows low-income households to cope with rising costs with prices up to 3,7 times lower in tense areas, but the level of construction of HLMs is insufficient and not fairly concentrated in areas with the highest demand;

- Resorting to off-plan housing, sometimes contested by some housing stakeholders, is a valuable tool for building low-cost housing in tight areas and promoting social diversity.

- In 2019, 54% of social housing was built off-plan, against only 3% in 2007.

- For the same land and construction costs, off-plan sales are more competitive than direct project management, with cost prices up to 6,1% lower

- The price cap on off-plan sales practiced by certain communities is counterproductive and limits the share of social housing in the programs.

“This study shows with impressive rigor the extent and gravity of the housing crisis that French society has been going through for decades. It also shows to what extent social housing is essential to meet the wide needs of the population of our country. More than ever, the mobilization for housing for all requires the use of all the tools available and in particular the VEFA which is a flexible and effective instrument to develop housing programs adapted to the specificities of each agglomeration ”declares Hervé Legros, president of the ALILA group.

"The success of social off-plan sales can easily be explained: it is the ideal lever for building more, denser, in the best places, at controlled costs and with more diversity"

Nicolas Bouzou, director of the Asterès cabinet

Main figures

Summary of the study

Changes in society are causing a multifaceted housing crisis

The study looks back on the changes that have taken place in society for 50 years and which have caused a structural change in demand:

- Certain attractive areas, such as dynamic metropolises in terms of employment and their outskirts, are experiencing an increase in demand and the need for new housing. In contrast, certain territories are characterized by an overall drop in demand, leading to an increase in the rate of vacant housing among the old stock.

- The increase in demand for housing is structurally greater than that of the population, in particular because of the phenomenon of decohabitation, that is to say the decrease in the average number of people living under the same roof (due to aging, the rise of celibacy, separations), which has absorbed 60% of housing construction since 1968.

- Households are looking for greater comfort, seeking to settle in the regions of the Atlantic and Mediterranean Arc, and having higher requirements in terms of quality of housing, with the development of individual housing and the increase in surface areas. habitable.

- However, more than other countries, France is characterized by the weak reaction of supply to demand: when the latter increases by 1,0%, the number of new dwellings increases by only 0,36%. (compared to 2% in the United States, and + 1% in Sweden), mainly due to the shortage of available land in the most tense areas, and competition with commercial real estate or second homes.

- As a result, the price of real estate grows faster than household income.

Social housing, which is a relevant response to this crisis, is having difficulty adjusting its offer in a tight zone.

- The social housing movement is a relevant response to the housing crisis and the rise in prices that it entails. It allows low-income households to find housing for prices up to 3,7 times lower than the market price in tense areas, but also to access property thanks to 13 disposals per year.

- But new social housing units are not very well built where the needs are: 53% of new social housing units are put into service in tight areas, while 73% of demand is concentrated there.

- As a result, waiting times are getting longer and the poorest households are excluded from the most desirable areas.

Faced with this difficulty, the VEFA is an effective lever to build faster and promote social diversity

- VEFA (Sale by private developers of housing in the future state of completion) is now the main mode of production of social housing, since in 2019, this mode of project management represented 54% of constructions, against 3 % only in 2007.

- The off-plan HLM, focused on social housing, makes it possible to build more quickly, thanks to lighter procedures. The savings made make it possible to acquire more sought-after and more expensive land.

- At the same time, private developers can develop social housing within large development projects comprising both shops and facilities, free housing and social housing. This is the principle of diffuse VEFA, which appears to be the best tool for enable local authorities to achieve the objective of social mix set by law, Solidarity and Urban Renewal (SRU) which imposes a minimum rate of 25% of social housing.

Excluding land charges, the cost of off-plan sales is lower than that of direct project management

- On a national average, the prices of the VEFA are higher than those of the MOD (Direct Project Management) but this can only be explained by the cost of land. Private developers build in more desirable areas and locations, with more expensive land to maximize the profit from the sale. Conversely, social landlords favor less expensive land, most often donated by local authorities or public establishments.

- For identical land and construction costs, off-plan sales are more competitive than direct project management, with cost prices that are 3,6% to 6,1% lower depending on the zone.

- This price difference is explained by two main factors:

- The financing conditions, which are more favorable for private developers since their projects are quickly amortized because they are intended for sale to a third party upon construction; the regulatory procedures followed by the MOD which affect costs and speed of execution (a architect takes 6 to 8 months).

- The difference in cost between VEFA and MOD allows the promoter to apply his commercial margin accordingly, without becoming more expensive than social landlords.

The price cap of off-plan public housing risks leading to a drop in social services

- The study also shows that the practice by local authorities of ceiling prices for off-plan housing, in the hope of reducing market prices, risks leading to a reduction in the volume of social services.

- In fact, the developers who are subject to this cap are not responsible for the evolution of the rise in market prices: the costs of land, buildings, and free-standing sales prices are imposed on them. Land prices are rising steadily, even when the economy slows down.

- Their margin level can only be slightly revised downwards since the banks refuse to grant their financing to projects which would not be profitable enough.

- The only rational consequence of capping the prices of off-plan HLM would be a reduction in the proportion of social housing that developers could build as part of a mixed project.

- The theoretical model constructed by Asterès quantifies the hypothesis of a decrease in the proportion of social housing for a given project.

- By applying this model to a sample of eight local authorities located in tense areas and which have effectively imposed ceiling prices 55% lower on average than those of free, Asterès figures at 27 points the possible drop in the number of social housing ( from 50 to 23%), for programs initially comprising as much free as social.

Selection of products

To read also

-

In France, stocks have proven to be the best investment over the last 40 years

In France, stocks have proven to be the best investment over the last 40 years

-

Since Covid-19, the temptation to live near the sea, according to a study

Since Covid-19, the temptation to live near the sea, according to a study

-

The average rate of real estate loans starts to fall again in the 1st quarter, according to Crédit Logement

The average rate of real estate loans starts to fall again in the 1st quarter, according to Crédit Logement

-

Old property prices are still falling but a recovery is taking shape

Old property prices are still falling but a recovery is taking shape

Popular News

-

A report on anticipating the effects of +4°C warming reaffirms the need for housing adaptation

A report on anticipating the effects of +4°C warming reaffirms the need for housing adaptation

-

AI is already revolutionizing businesses in architecture, engineering, construction... according to Autodesk's "State of Design & Make" study

AI is already revolutionizing businesses in architecture, engineering, construction... according to Autodesk's "State of Design & Make" study

-

The slowdown in the decline in mortgage rates continues

The slowdown in the decline in mortgage rates continues

-

What steps for an efficient energy transformation of the building?

What steps for an efficient energy transformation of the building?

Publi-editorial

-

Glass pergola: enjoy its outdoor spaces with elegance and modernity all year round

Glass pergola: enjoy its outdoor spaces with elegance and modernity all year round

-

Hydro'Way, Eco'Urba, StabiWay and Baltazar... permeable floor covering solutions from JDM Expert

Hydro'Way, Eco'Urba, StabiWay and Baltazar... permeable floor covering solutions from JDM Expert

-

Cero IV minimalist sliding door by Solarlux: light as the protagonist

Cero IV minimalist sliding door by Solarlux: light as the protagonist

-

EduRénov Plan: Rockwool unveils its Guide to successful energy renovation of school buildings

EduRénov Plan: Rockwool unveils its Guide to successful energy renovation of school buildings